The solar loan vs personal loan decision is the single biggest financing question a homeowner faces before committing to rooftop solar in 2026. The headline gap is wide: dedicated solar loans run 8.5%–12% per annum while personal loans sit at 11%–18%: a 2.5–6 percentage-point spread that compounds into roughly ₹28,000 of extra interest on a typical 5 kW system financed over five years. Solar loans, however, come with a non-negotiable condition, the installer must be MNRE-empanelled (Ministry of New and Renewable Energy) and the panels must sit on the ALMM (Approved List of Models and Manufacturers) register. Personal loans carry no such restriction, but the higher interest rate erodes the very savings rooftop solar is meant to produce. For most residential buyers, the rate gap wins the argument; for a small minority, speed and flexibility tip it the other way.

This guide walks through the five variables that actually decide the choice, side-by-side EMI (Equated Monthly Instalment) numbers for a 5 kW system, the lender list for both categories, and the situations where a personal loan genuinely outperforms a solar loan. We also flag the most expensive mistake we see, borrowers picking a personal loan for speed, then losing the ₹78,000 PM Suryaghar subsidy because their installer wasn’t MNRE-empanelled.

Direct answer. For rooftop solar in 2026, a solar loan is better than a personal loan for most residential buyers: solar loan rates run 8.5%–12% with tenure up to 84 months, while personal loans charge 11%–18% over 60 months. On a ₹2 lakh, 5-year loan that gap saves around ₹28,000 in total interest. Personal loans only win when the loan size is under ₹50,000, when documentation is weak, or when you need disbursal in under 72 hours.

If you have a clean salary slip, a CIBIL (Credit Information Bureau India Limited) score above 720, and time to wait 5–10 working days for sanction, the solar loan is almost always the cheaper route. Read on for the side-by-side maths.

Why This Decision Matters, Total Interest Over 5 Years

Rooftop solar is, at its core, a financial product disguised as an electrical installation. You’re swapping a recurring utility bill for a fixed asset, and the cheapness of that swap depends on two numbers: the system cost and the cost of the money you borrow to buy it. The first is largely fixed by panel and inverter prices; the second is entirely a function of which loan you choose.

A 5 kW residential system in 2026 costs roughly ₹2.85 lakh before subsidy and ₹2.07 lakh after the ₹78,000 PM Suryaghar subsidy. Most homeowners finance the post-subsidy cost, about ₹2 lakh, through a bank or NBFC (Non-Banking Financial Company). Over a 5-year tenure, that ₹2 lakh principal generates ₹54,000 in interest at 10% (solar loan) but ₹82,000 in interest at 14% (personal loan): a delta of ₹28,000 that the borrower keeps or hands to the lender depending entirely on the loan category chosen.

Stretch the comparison to a 7-year solar loan (84 months at 9.5%) versus the maximum 60-month personal loan and the gap widens further. The longer tenure on a solar loan also drops the monthly EMI, freeing cash flow for other expenses or pre-payments. Personal loans rarely extend beyond 60 months for unsecured borrowers, capping the relief on monthly cash flow.

The other dimension is the PM Suryaghar subsidy itself. Under the Ministry of New and Renewable Energy (MNRE) rules, the ₹78,000 subsidy disburses only if the installer is on the empanelled list at pmsuryaghar.gov.in and the components are ALMM-registered. A personal loan lets you fund any installer, including non-empanelled ones, but the moment you do, the subsidy is forfeited. That single error converts a “small rate premium” personal loan into a “₹78,000 net loss” personal loan. The category decision and the subsidy decision are linked, even though they sit in different parts of the buying journey.

The 5-Variable Solar Loan vs Personal Loan Decision Matrix

This is the framework we walk residential buyers through before they sign any financing document. Five variables, weighted by their actual rupee impact, decide which loan category fits a given borrower. Walk through each row honestly and the answer falls out, there’s no judgement call left at the end.

| Variable | Solar Loan | Personal Loan | Weight |

|---|---|---|---|

| Interest rate | 8.5%–12% p.a. | 11%–18% p.a. | High, ₹15K–₹40K impact |

| Tenure | Up to 84 months | Up to 60 months | Medium, monthly EMI relief |

| Processing fee | 0.5%–1% of loan | 1%–2% of loan | Low, ₹1K–₹3K impact |

| Documentation | KYC (Know Your Customer) + income + MNRE installer quote + Suryaghar reference | KYC + income only | Medium, decides approval speed |

| Vendor restriction | MNRE-empanelled only (ALMM + BIS) | Any installer | High, subsidy risk |

Variable 1, Interest rate. This is where the rupee gap lives. Solar loans are priced cheaper because the lender holds an indirect security (the panel installation, sometimes covered by a hypothecation note) and because public-sector banks have priority sector lending (PSL) targets that solar loans help satisfy. Personal loans are fully unsecured, so the rate prices in default risk. The 2.5–6 percentage point gap is structural, not promotional.

Variable 2, Tenure. Solar loans run up to 84 months across most lenders; SBI’s Surya Ghar product allows 120 months for select borrowers. Personal loans typically cap at 60 months, with 72 months only for prime salaried customers at a few private banks. The longer tenure compresses your EMI by roughly ₹1,000/month on a ₹2 lakh principal, useful if cash flow is tight.

Variable 3, Processing fee. Both categories charge a one-time fee at disbursal. Solar loans average 0.5%–1%; personal loans 1%–2%. On a ₹2 lakh loan the rupee gap is ₹1,000–₹3,000, not large in absolute terms, but a reliable indicator that the lender treats the loan as lower-risk.

Variable 4, Documentation. Personal loans need only KYC and an income document (salary slip or ITR). Solar loans add two extras: a quote from an MNRE-empanelled installer and the PM Suryaghar application reference number. If you don’t have an installer shortlisted or haven’t started the Suryaghar process, expect a 5–10 day approval delay while these are collected.

Variable 5, Vendor restriction. This is the dealbreaker for some buyers. A solar loan locks you into MNRE-empanelled installers with ALMM-listed panels and BIS-certified (Bureau of Indian Standards) inverters. A personal loan has zero vendor restriction. The trap: many homeowners interpret “no vendor restriction” as freedom, until they realise that vendor restriction is also what protects subsidy eligibility. Picking a non-empanelled installer with personal loan money forfeits the ₹78,000 PM Suryaghar subsidy, which dwarfs any interest saving.

Solar Loan, Lower Rate, MNRE Vendor Restriction

A solar loan is a purpose-built consumer loan where the lender disburses funds either directly to the installer or to the borrower against installer invoices. In India in 2026, the major solar loan providers are State Bank of India (SBI Surya Ghar at 9.5%), HDFC Bank Solar Loan at 9.5%, ICICI Bank at 10%, Tata Capital at 10.5%, and Bajaj Finance at around 12.5% on its dedicated rooftop solar product. The Indian Renewable Energy Development Agency (IREDA) also runs a refinance line that supports several of these lenders.

The structural advantages of a solar loan flow from three sources. First, priority sector lending status: rooftop solar loans count toward the public-sector banks’ renewable energy PSL targets, which pushes them to keep rates competitive. Second, lower perceived default risk: borrowers funding solar tend to be homeowners with bill payment history, a population the lender already trusts. Third, subsidy linkage: the PM Suryaghar subsidy can be applied directly against the loan balance at most lenders, reducing the borrower’s effective principal by ₹78,000 within 60–90 days of commissioning.

The restrictions are equally structural. The lender will only release funds for ALMM-listed panels and BIS-certified inverters, and only against an invoice from an installer who appears on the PM Suryaghar empanelled vendor list. This is the same condition that the subsidy itself requires, so for any buyer planning to claim the ₹78,000 the restriction is invisible, they were going to use an empanelled installer anyway.

Approval timelines run 5–10 working days at most banks. SBI tends to be slowest (8–12 days); HDFC and ICICI move faster (4–7 days) for existing customers with pre-approved limits. NBFCs like Tata Capital and Bajaj Finance can sanction in 3–5 days but charge 100–200 basis points more. Compare the specific lenders side by side in our SBI Surya Ghar loan guide, ICICI solar loan guide, Tata Capital solar loan guide, and Bajaj Finserv solar loan guide.

Tip, stack the subsidy against the loan

At SBI, HDFC, and ICICI you can request that the ₹78,000 PM Suryaghar subsidy be credited directly against the outstanding loan balance once the Direct Benefit Transfer arrives. This drops your principal by ~40% on a 5 kW loan, shortens the tenure, and saves a further ₹8,000–₹12,000 in interest over the loan life. Ask for "subsidy adjustment against principal" at sanction.

Personal Loan, Higher Rate, Any Vendor

A personal loan is an unsecured consumer credit product disbursed against income and credit score alone. It carries no end-use restriction, you can spend the money on a wedding, a medical bill, or a solar installation. In 2026, personal loan rates for salaried borrowers with CIBIL above 750 run 12%–14% at private banks (HDFC 13%, ICICI 12.5%) and 11%–13% at public-sector banks (SBI 12.5%). NBFCs like Bajaj Finance price personal loans at 14%–18% depending on borrower profile.

The advantages of a personal loan are speed and flexibility. Pre-approved customers at HDFC, ICICI, and Axis can get disbursal in 24–72 hours with fully digital onboarding. Documentation is limited to PAN (Permanent Account Number), Aadhaar, salary slip, and bank statement, no installer quote, no Suryaghar application reference, no ALMM verification. For a buyer who has already shortlisted an installer and wants the panel on the roof in three weeks, a personal loan compresses the financing path from 10 days to 2.

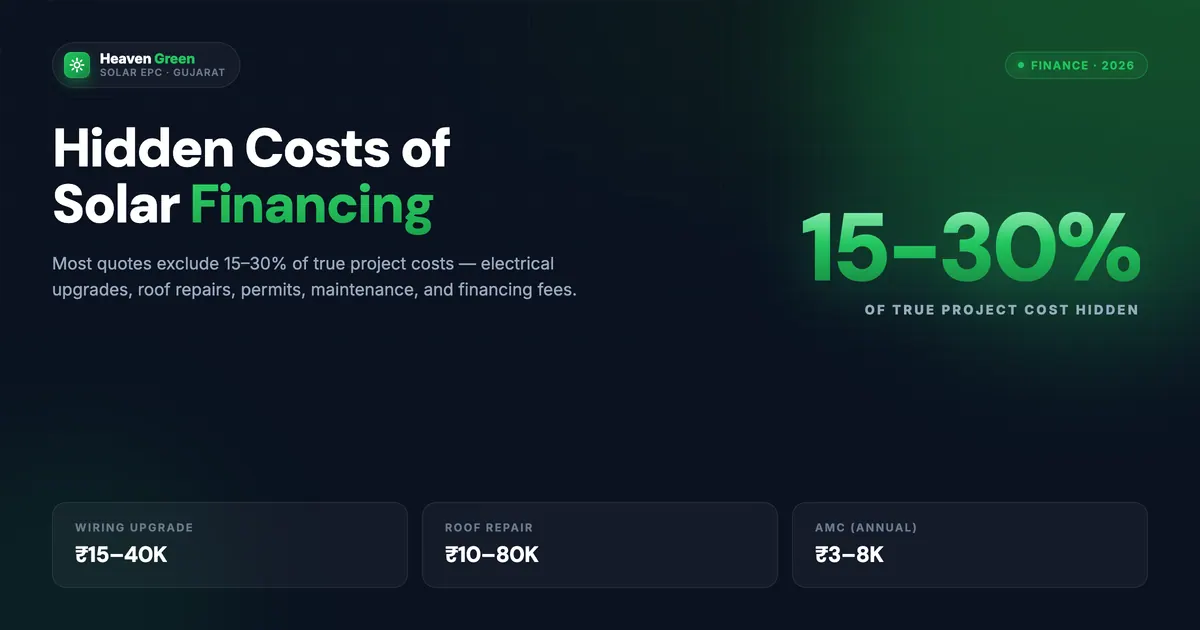

The disadvantages are equally real. The interest rate gap of 2.5–6 percentage points translates to ₹15,000–₹40,000 of extra interest over a 5-year, ₹2 lakh loan. Tenure caps at 60 months at most lenders, which keeps the monthly EMI ₹800–₹1,200 higher than the equivalent solar loan. Processing fees run higher (1%–2%) and prepayment penalties can apply on fixed-rate personal loans during the first 12 months.

The most dangerous trap with personal loans is the subsidy forfeiture risk. A personal loan has no vendor restriction, which means it can fund a non-MNRE installer. Some buyers, confused by this freedom, pick a cheaper non-empanelled installer to offset the higher interest rate, then discover the ₹78,000 PM Suryaghar subsidy is unavailable. The net financial outcome is dramatically worse: 6% higher interest cost on the loan plus ₹78,000 of forfeited subsidy. Always confirm the installer is on the PM Suryaghar empanelled list before signing a personal loan, regardless of which lender you’re using.

Get a free solar financing review. Our team maps your CIBIL score, salary band, and target system size against the live rate cards from SBI, HDFC, ICICI, Tata Capital, and Bajaj, and tells you whether a solar loan or personal loan saves more rupees over the life of the loan. Get your free quote →

EMI Side-by-Side for 5 kW Solar

Numbers settle this discussion faster than commentary. Below is the EMI comparison for a 5 kW residential system financed at the post-subsidy cost of ₹2 lakh, the most common scenario in our 2026 installation book. We’ve used the rate midpoints for both categories (10% solar loan, 14% personal loan) and the maximum tenure each category typically allows.

| Scenario | Loan amount | Rate | Tenure | Monthly EMI | Total interest | Total payable |

|---|---|---|---|---|---|---|

| Solar loan (HDFC/SBI/ICICI) | ₹2,00,000 | 10% p.a. | 60 months | ₹4,249 | ₹54,940 | ₹2,54,940 |

| Solar loan, longer tenure | ₹2,00,000 | 10% p.a. | 84 months | ₹3,320 | ₹78,890 | ₹2,78,890 |

| Personal loan (private bank) | ₹2,00,000 | 14% p.a. | 60 months | ₹4,653 | ₹79,180 | ₹2,79,180 |

| Personal loan (NBFC) | ₹2,00,000 | 16% p.a. | 60 months | ₹4,862 | ₹91,720 | ₹2,91,720 |

The cleanest comparison is row 1 vs row 3, same ₹2 lakh principal, same 60-month tenure, only the rate differs. The solar loan saves ₹24,240 in total interest, or roughly ₹404 per month of cash flow. Stretch the solar loan to 84 months (row 2) and the monthly EMI drops to ₹3,320, ₹1,333 less than the personal loan EMI, but total interest rises to ₹78,890. Most borrowers should pick row 1 for the lowest absolute cost; pick row 2 only if monthly cash flow is the binding constraint.

The NBFC personal loan in row 4 is the worst outcome for nearly every buyer profile. It exists because NBFCs approve borrowers with weaker credit history that banks reject, but for any borrower with CIBIL above 720, a bank solar loan should always be the starting point. See the full breakdown by system size in our solar loan EMI for 3 kW / 5 kW / 10 kW guide.

For buyers who can’t bring 20% down payment, our zero-down-payment solar guide covers the 100%-financed structures available at SBI and Tata Capital.

When Personal Loan Actually Wins

The honest answer to “solar loan or personal loan” isn’t a universal verdict, there are three specific situations where the personal loan is genuinely the better choice, and pretending otherwise would mislead borrowers. Here’s when to break the default rule.

| Situation | Why personal loan wins |

|---|---|

| Loan amount under ₹50,000 | Processing overhead + documentation effort of a solar loan exceeds the ₹3,000–₹5,000 interest savings; personal loan disburses in 48 hours |

| Weak income documentation | Solar loans require formal salary slip or ITR; personal loans accept bank statements alone at some NBFCs |

| Urgency (under 72 hours) | Solar loans take 5–10 days minimum; pre-approved personal loans disburse same-day |

| Already-installed non-empanelled system | Solar loan won’t refinance a non-MNRE installation; personal loan will |

| Top-up over existing loan | Personal loan top-ups disburse against the existing relationship in 24 hours |

Loan under ₹50,000. For a 1 kW system costing ₹35,000–₹45,000 after subsidy, the absolute interest saving from a solar loan over 24 months is roughly ₹3,000–₹4,000. Against that, you bear the documentation effort and 5–10 day wait. A personal loan with a 24-hour digital sanction trades ₹3,000 of interest for two weeks of your time, a reasonable swap for most working professionals.

Weak documentation. Self-employed buyers without consistent ITR filings, gig workers, or small-business owners with cash-heavy income find solar loans hard to qualify for. Bank solar loans want salary slips or two years of ITRs; NBFCs running personal loans against bank statement velocity (Flexi Loan, KreditBee-style products) are more accommodating. The 3–4 percentage point rate premium is the cost of access.

True urgency. Some buyers face seasonal triggers, pre-monsoon roof commissioning, the end of a financial year tax window, or a state-level subsidy expiry. If sanction must close in 48–72 hours, a pre-approved personal loan from an existing bank relationship is the only product that delivers. The solar loan can’t compress its document collection and feasibility checks below 5 working days.

In each of these cases, always still pick an MNRE-empanelled installer even though the personal loan doesn’t require it. That preserves the ₹78,000 Suryaghar subsidy, which is independent of the loan category.

Common Mistakes Borrowers Make Choosing

These are the six recurring errors we see across our financing consultations in 2026. Each one costs the borrower real money, sometimes more than the entire interest gap the loan category was supposed to optimise. Run through this list before you sign.

-

1

Picking a personal loan for speed, then choosing a non-empanelled installer. The ₹78,000 PM Suryaghar subsidy disappears. Even at a 6% rate premium, no personal loan can recover that loss. Always use an MNRE-empanelled installer regardless of loan type.

-

2

Ignoring the longer tenure on a solar loan. Borrowers default to a 60-month tenure out of habit. Solar loans up to 84 months drop the monthly EMI ₹900–₹1,200, useful if cash flow is tight, even if total interest rises.

-

3

Not requesting subsidy adjustment against the loan principal. The ₹78,000 DBT can be applied directly to the loan balance at SBI, HDFC, and ICICI. Without an explicit request, the lender treats it as a regular credit and you keep paying EMIs on the full original balance.

-

4

Comparing flat rates to reducing balance rates. Some NBFC personal loans quote flat interest (e.g., 8% flat) that converts to ~14.5% reducing balance. Always confirm the rate type before signing, the effective annualised rate is what matters.

-

5

Skipping the processing fee and prepayment penalty fine print. A 2% processing fee on a ₹3 lakh loan is ₹6,000, equivalent to 3 months of interest. Prepayment penalties on personal loans can lock you in for 12 months even if you receive a windfall.

-

6

Borrowing the gross system cost instead of the post-subsidy cost. If you finance ₹2.85 lakh and then receive the ₹78,000 subsidy as a separate credit, you've paid 3 months of unnecessary interest on the subsidy portion. Borrow ₹2.07 lakh and bridge the subsidy with a short-term overdraft if needed.

Watch out, the 100% financing trap

Some installers advertise "zero down payment, 100% finance" through a tie-in personal loan at the higher 14% rate. The convenience is real, but you're paying 4% extra on the full system cost for 5 years. On a 5 kW system, that's an extra ₹35,000–₹40,000 the installer's quoted price doesn't show. Always model the all-in finance cost separately from the system cost before signing.

Solar Loan vs Personal Loan, Quick Verdict

- + Lower interest rate (8.5%–12%)

- + Tenure up to 84 months

- + Lower processing fee (0.5%–1%)

- + Subsidy can adjust against principal

- + Forces ALMM + BIS quality components

- + Saves ₹15K–₹40K interest over 5 years

- - Approval takes 5–10 working days

- - Locked into MNRE-empanelled installers

- - Needs installer quote + Suryaghar reference

- - Some banks restrict to specific brand panels

- - Salary/ITR documentation mandatory

- - Hypothecation creates a charge on the system

- + Disbursal in 24–72 hours for pre-approved

- + KYC + income documents only

- + No vendor or component restriction

- + Fully digital onboarding

- + Works for under-₹50K loan amounts

- + Accepts weaker documentation profiles

- - Higher interest rate (11%–18%)

- - Tenure capped at 60 months

- - Higher processing fee (1%–2%)

- - Risk of subsidy forfeiture via non-empanelled installer

- - Prepayment penalty in year 1 at some lenders

- - Costs ₹28K extra interest on typical ₹2L, 5-yr

Verdict. For any rooftop solar buyer financing ₹1 lakh or more with a CIBIL score above 720 and 5–10 days to wait for sanction, a solar loan is the better choice, every time. The 2.5–6 percentage point rate gap, the 24-month tenure extension, and the ability to apply the ₹78,000 subsidy directly to the principal make it the cheaper money. Personal loans win only at small ticket sizes, weak documentation, or hard urgency. And in all cases, always use an MNRE-empanelled installer regardless of loan category, the subsidy depends on it.

How Heaven Green Energy Coordinates Loan Selection

Heaven Green Energy is MNRE-empanelled across Rajasthan and partners with all five major solar loan providers, State Bank of India, HDFC Bank, ICICI Bank, Tata Capital, and Bajaj Finance. Our finance desk reviews each buyer’s CIBIL score, salary documentation, and target system size, then surfaces the live rate cards from each lender so you can compare like-for-like.

What we handle on the financing side, in sequence:

- CIBIL and rate profiling: pull your score (with consent) and map it to the rate cards each lender will actually quote, not the headline marketing rate.

- Solar loan paperwork: installer quote, MNRE empanelment certificate, ALMM listing for panels, BIS certification for inverter, and PM Suryaghar reference number all bundled into the loan file.

- Subsidy-against-principal request: drafted at sanction so the ₹78,000 DBT lands directly on the loan balance, not your savings account.

- Personal loan fallback: if solar loan timelines don’t fit, we coordinate a pre-approved personal loan with a bank where you already have a relationship.

- Documentation pre-check: eliminates the rejection patterns we see most often (income mismatch, address inconsistency, CIBIL old-write-off flags).

Explore the services and tools that fit your buying stage:

- Residential Solar: 1–10 kW rooftop systems with full PM Suryaghar and loan coordination.

- Solar Calculator: model your subsidy, loan EMI, and payback for your bill in under 60 seconds.

- Channel Partner Programme: for installers and dealers who want to offer financed solar to their customers.

- Contact Us: speak with the finance desk for a no-obligation rate comparison.

For the deeper lender-specific reviews, see our HDFC solar loan guide, SBI Surya Ghar loan guide, ICICI solar loan guide, Tata Capital solar loan guide, and Bajaj Finserv solar loan guide.

Frequently Asked Questions

Is a solar loan always cheaper than a personal loan for rooftop solar?

For nearly every borrower with a CIBIL score above 720 and a loan size of ₹1 lakh or more, yes, a solar loan is cheaper. The 2.5–6 percentage point rate gap saves ₹15,000–₹40,000 in total interest over a 5-year tenure on a typical ₹2 lakh principal. The exceptions are small loan sizes (under ₹50,000), borrowers with weak income documentation, and situations where disbursal must close in under 72 hours. In those three cases the personal loan’s speed and flexibility offset the rate premium.

Can I get a personal loan and still claim the ₹78,000 PM Suryaghar subsidy?

Yes, the PM Suryaghar subsidy is tied to the installer and components, not to the loan type. As long as your installer is MNRE-empanelled and uses ALMM-listed panels with BIS-certified inverters, the ₹78,000 subsidy disburses regardless of whether you funded the system through a solar loan, personal loan, or your own savings. The trap to avoid is using personal loan freedom to pick a non-empanelled installer, that forfeits the subsidy.

What CIBIL score do I need for a solar loan in 2026?

Public sector banks like SBI sanction solar loans at CIBIL scores from 700, with the best rates reserved for 750 and above. Private banks (HDFC, ICICI) typically want 720 minimum, and NBFCs like Tata Capital and Bajaj Finance go down to 680 with a rate premium of 100–200 basis points. Below 680, most lenders decline the solar loan and the borrower has to fall back on a personal loan or NBFC consumer loan at 16%–22%, which usually makes the project economics unattractive.

How long does a solar loan take to disburse compared to a personal loan?

Solar loans take 5–10 working days at most banks; SBI averages 8–12 days, HDFC and ICICI close in 4–7 days for existing customers, and NBFCs like Tata Capital and Bajaj Finance disburse in 3–5 days. Personal loans for pre-approved bank customers disburse in 24–72 hours; non-pre-approved applications take 3–5 days. If timing isn’t critical, the solar loan’s lower rate is worth the extra week of wait.

Can the PM Suryaghar subsidy be applied directly to my loan balance?

Yes, at most major solar loan providers, SBI, HDFC, and ICICI all support a “subsidy adjustment against principal” instruction at sanction. When the ₹78,000 Direct Benefit Transfer lands in your Aadhaar-linked account, it can be auto-debited to the loan account and reduce the principal balance. This shortens the effective tenure or lowers the EMI and saves an additional ₹8,000–₹12,000 in interest over the life of the loan. You must explicitly request this at sanction; it’s not automatic.

What’s the maximum tenure available on a solar loan in 2026?

Most lenders cap solar loan tenure at 84 months (7 years). SBI Surya Ghar allows 120 months (10 years) for select borrower profiles, particularly salaried customers with higher loan amounts. Personal loans cap at 60 months for the same borrower at almost every lender, with 72 months available only for prime customers at a few private banks. The longer solar loan tenure compresses the monthly EMI by ₹900–₹1,200 on a ₹2 lakh principal, useful if cash flow is tight.

Are solar loans tax deductible in India?

Solar loans for residential rooftop systems do not qualify for a specific interest deduction under the current Income Tax Act, but the system itself may qualify for accelerated depreciation if installed at a commercial property. For salaried residential buyers, the financial benefit is captured in the lower interest rate and the PM Suryaghar subsidy, not in tax deductions. Self-employed buyers with a home-office component may be able to claim partial depreciation through their business return, consult a chartered accountant for specifics.

Should I take the maximum tenure on a solar loan to lower my EMI?

Only if monthly cash flow is genuinely tight. The longer the tenure, the higher the total interest you pay, at 10%, stretching a ₹2 lakh loan from 60 months to 84 months drops the EMI from ₹4,249 to ₹3,320 (₹929 cash flow relief per month) but raises total interest from ₹54,940 to ₹78,890 (₹23,950 extra cost). For buyers with stable salary, the 60-month tenure is the right default. For borrowers with variable income or other large EMIs already, the 84-month option is the cash flow safety valve.

What happens if I lose my job during a solar loan tenure?

Solar loans don’t carry employment-linked acceleration clauses, your EMI obligation continues regardless of employment status. If you fall behind, the lender first attempts restructuring (EMI moratorium, tenure extension), then triggers the hypothecation charge on the panel installation as a last resort. In practice, residential solar loan default rates run below 1% across major lenders. Maintain 3–6 months of EMI as a reserve and you’ll absorb most income disruptions without distress.

Can I prepay a solar loan without penalty?

At most banks, yes, solar loans on floating interest rates carry no prepayment penalty under RBI guidelines for individual borrowers. Fixed-rate solar loans may charge 2%–4% if prepaid within 12 months of disbursal. Personal loans more commonly carry prepayment penalties in the first year, regardless of rate type. If you expect a windfall (bonus, ITR refund, asset sale) within the first year, confirm the prepayment clause before signing, it’s the most overlooked term in the loan agreement.