Indian electricity tariffs have risen 3.5–5.5% every year for the last decade. That is not a forecast, that is the Central Electricity Authority (CEA) tariff bulletin record from 2014 to 2024 across the country’s largest DISCOMs. If you are paying ₹8.50 per kWh (kilowatt-hour) for grid electricity today, the same unit costs you ₹12.50 in ten years and ₹18 in twenty. Solar flips that compounding curve in your favour: once your system is paid back, your generation cost is locked at zero, the AMC (Annual Maintenance Contract) sits at ₹2,000–₹5,000 a year, and every future tariff hike becomes savings on your side of the ledger rather than expense on the DISCOM’s.

This guide does the bill-insulation math properly, state-by-state historical hike data, the 25-year cumulative bill with and without solar, the four variables that decide your real ROI (Return on Investment), and the sensitivity table that shows why a tariff hike accelerates rather than threatens your solar payback.

Direct answer. Indian electricity tariffs rose 3.5–5.5% per year on average between 2014 and 2024 per CEA data. A residential rooftop solar system in 2026 locks your generation cost at an LCOE (Levelised Cost of Energy) of ₹2.50–₹3.50/kWh for 25 years, flat. Every 1% additional tariff hike compresses solar payback by roughly six months, so escalation makes the investment stronger, not weaker. With solar, your bill stops compounding.

If you have ever stared at a DISCOM bill that crept up 8% in one cycle and wondered whether the tariff “stabilises”, the honest answer is no. Tariff stability is a political talking point, not an engineering reality. Coal pricing, transmission losses, renewable purchase obligations, and DISCOM losses all feed escalation. The only consumer-side hedge that pays in rupees rather than promises is owning your generation.

India’s Electricity Tariff Hike History 2014-2024 by State

Aggregated from Ministry of Statistics and Programme Implementation (MoSPI) electricity consumption index and state regulator tariff orders, the picture is uniform: every major state has compounded residential tariffs at 3–6% per year. Some did it openly through annual tariff orders; some did it quietly through fuel-cost adjustment surcharges that show up as extra lines on your bill.

| State / DISCOM | Residential CAGR 2014-24 | Commercial CAGR | Decadal cumulative (residential) |

|---|---|---|---|

| Maharashtra (MSEDCL) | 4.5% | 5.2% | ~55% |

| Gujarat (DGVCL/MGVCL) | 3.2% | 4.0% | ~37% |

| Uttar Pradesh (UPPCL) | 4.8% | 5.5% | ~60% |

| Tamil Nadu (TANGEDCO) | 5.5% | 6.0% | ~71% |

| Karnataka (BESCOM) | 3.8% | 4.5% | ~45% |

| Delhi (BSES Rajdhani) | 3.5% | 4.2% | ~41% |

| Rajasthan (JVVNL) | 4.2% | 5.0% | ~51% |

| Telangana (TSSPDCL) | 4.0% | 4.8% | ~48% |

Sources: MERC tariff orders, GERC tariff orders, TNERC and KERC retail tariff filings, BSES Rajdhani retail orders 2014–2024. CAGR (Compound Annual Growth Rate) computed on lowest-slab and highest-slab residential energy charges; commercial CAGR uses LT (Low Tension) commercial category.

Two patterns stand out. First, no state shows zero or negative escalation, even Gujarat, the cheapest of the lot, still compounded at 3.2%. Second, commercial tariffs escalate faster than residential, because residential subsidisation is politically protected and gets cross-subsidised by commercial and industrial categories.

The Tariff-Hike Insulation Math, 4 Variables

This is the framework we walk every customer through before they sign. It is a four-variable model: hold three constant and any one tells you whether solar makes sense at your specific bill. We call it The Tariff-Hike Insulation Math, 4 Variables because once you have these four numbers, you do not need a calculator or an Excel model; the answer is mechanical.

Variable 1, Current Tariff (T₀). The blended ₹/kWh you pay today, including energy charge, fuel surcharge, electricity duty, and fixed charges divided by your monthly consumption. For most urban Indian homes this lands at ₹7–₹10/kWh; for commercial connections ₹9–₹13/kWh. Pull it from your last three bills and average, single-month snapshots mislead.

Variable 2, Escalation Rate (e). The annual tariff hike. Use 4% as a base assumption for residential and 5% for commercial unless you have a specific reason to deviate (UP and TN should use 5% residential; Gujarat can use 3.5%). This is the variable consumers most often set to zero in their mental math, and that single error is what understates solar value by 30–40%.

Variable 3, System LCOE. The Levelised Cost of Energy of your solar system over 25 years. For a residential rooftop in 2026, with PM Suryaghar subsidy applied and standard inverter replacement budgeted at year 12, this lands at ₹2.50–₹3.50/kWh. For commercial systems with Accelerated Depreciation taken in years 1–2, ₹2.80–₹3.80/kWh. This number stays flat for the system’s life, that is the entire point of bill insulation.

Variable 4, Ownership Horizon (H). How long you intend to own the property or stay on this connection. For owned homes, this is usually 15–25 years and the math becomes overwhelmingly pro-solar. For rented or short-tenure cases, the math weakens, and we say so honestly.

Framework cheat

If T₀ > LCOE × 2 and e > 3% and H > 7 years, solar always wins on rupee math. The interesting cases, where you should actually run numbers, are when T₀ < ₹6/kWh (subsidised slabs) or H < 5 years (planning to sell). Everything else is a yes.

The compounding asymmetry is the real story. T₀ × (1+e)^H grows on the grid side; LCOE stays flat on the solar side. Over a 25-year ownership horizon at 4% escalation, the grid bill grows to 2.67× its starting value. Solar’s LCOE growth: 0%.

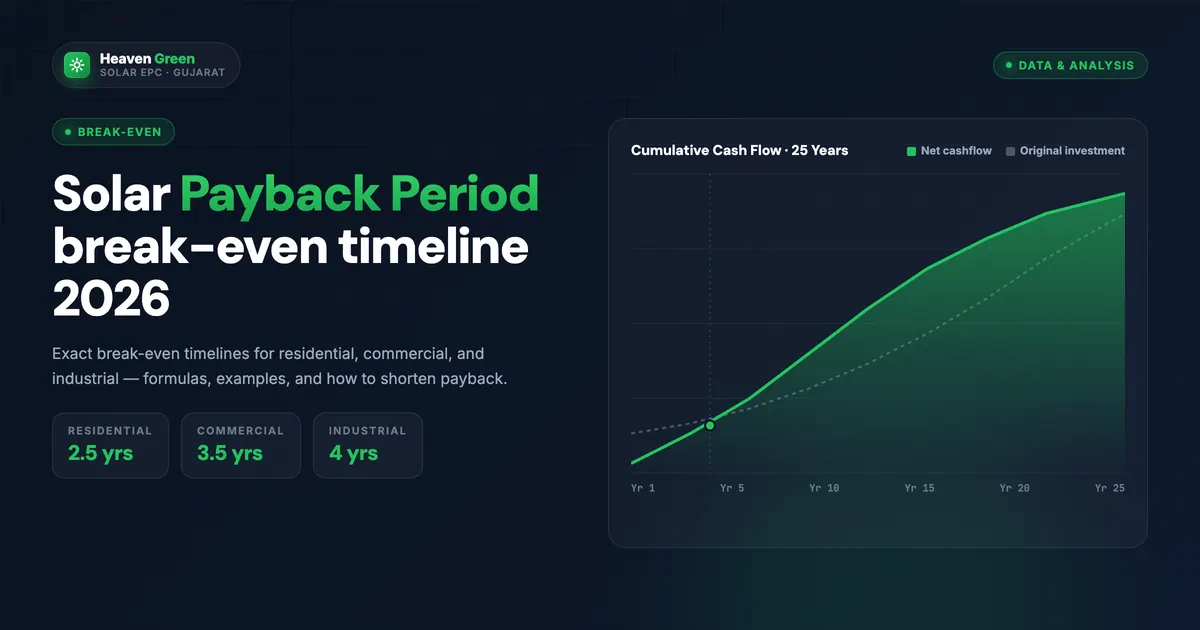

25-Year Cumulative Bill, With vs Without Solar

Take a typical Pune household consuming 600 kWh/month at MSEDCL’s current blended residential tariff of ₹9.20/kWh. Annual electricity spend today: ₹66,240. Now project forward with 4% annual escalation versus a 5 kW solar system at LCOE ₹3.00/kWh (residential, post-subsidy).

| Year | Without solar (₹) | With solar, 5 kW (₹) | Annual differential |

|---|---|---|---|

| Year 1 | 66,240 | 21,600 + 6,000 capex amort | ~38,640 |

| Year 5 | 77,484 | 21,600 + 6,000 | ~49,884 |

| Year 10 | 94,284 | 21,600 + 4,000 (post-payback AMC) | ~68,684 |

| Year 15 | 1,14,720 | 5,000 (AMC + replacement provision) | ~1,09,720 |

| Year 20 | 1,39,584 | 5,500 | ~1,34,084 |

| Year 25 | 1,69,818 | 6,000 | ~1,63,818 |

| 25-yr total | ₹27.6 lakh | ₹4.8 lakh (incl. capex) | ₹22.8 lakh saved |

Without solar at 4% escalation, the 25-year cumulative bill grows ~68% in compounded terms and the total cash out is ₹27.6 lakh in nominal rupees. With solar, total cash out, including the ₹2.85 lakh post-subsidy system cost, lifetime AMC, and an inverter replacement in year 12, is ₹4.8 lakh. The bill-insulation differential is ₹22.8 lakh over 25 years on a single 5 kW residential system.

The number people miss is what happens after Year 6 payback. From year 7 onward, the “cost” of solar generation is essentially just AMC, ₹4,000–₹5,000 a year for cleaning and minor service. Every rupee of tariff hike from year 7 to year 25 is pure savings. This is the locked-rate effect: you bought a 25-year supply contract at one fixed price.

For the year-by-year cash flow specific to your bill, run the Heaven Green solar calculator, it bakes in a 4% default escalation, the Maharashtra slab structure, and the PM Suryaghar subsidy.

How Tariff Hikes Accelerate Solar Payback

The counter-intuitive piece, and the one that flips most “solar is risky” objections, is that tariff hikes make payback faster, not slower. This is because your annual savings (which fund the payback) are pegged to the grid tariff, while your cost (LCOE) is pegged to nothing.

| Annual tariff hike assumption | 5 kW payback (residential) | Payback delta vs base |

|---|---|---|

| 0% (flat tariff, hypothetical) | 6.8 years | +1.6 years slower |

| 2% | 5.8 years | +0.6 years slower |

| 3% | 5.4 years | +0.2 years slower |

| 4% (base case) | 5.2 years | baseline |

| 5% | 4.6 years | -0.6 years faster |

| 6% | 4.2 years | -1.0 years faster |

The rule of thumb that comes out of this: every 1% additional tariff escalation compresses payback by roughly six months on a 5 kW residential system. For 10 kW residential the effect is slightly larger (~7 months per 1%); for commercial systems with AD applied, ~4 months per 1% because the depreciation tax shield front-loads the recovery.

So when a relative tells you “tariffs might fall, then your solar payback breaks”, the data says the opposite is the real risk. The historical base rate of falling tariffs in India is zero observations across 30+ years. The base rate of 3–6% hikes is virtually every year. You are hedging the high-probability outcome.

For the deeper mechanics of how tariff escalation interacts with the payback curve, see solar payback period and the Solar ROI calculation guide.

Free tariff-adjusted ROI report. Our engineers run your last three DISCOM bills through the 4-variable model and send back a year-by-year cash flow at 3%, 4%, and 5% escalation scenarios. Get your free quote →

State-by-State Tariff Trend (Maharashtra, Gujarat, UP, TN, Karnataka)

Granular state behaviour matters because the LCOE of your solar system is roughly the same nationwide (irradiance varies, but not as much as tariff), so the state-by-state tariff trajectory is what changes the rupee outcome.

Maharashtra (MSEDCL): 4.5% residential CAGR 2014–24 per MERC tariff orders. The 2024 order added 5.5%, above the historical average, and the fuel cost adjustment surcharge added another 30 paise. MSEDCL residential blended tariffs now sit at ₹8.80–₹10.20/kWh for medium consumers. Solar payback in Maharashtra has compressed from 6.2 years in 2019 to 4.8 years in 2026 thanks to compounding hikes plus PM Suryaghar.

Gujarat (DGVCL/MGVCL/PGVCL): 3.2% residential CAGR, the lowest of the major states. Gujarat keeps residential tariffs low through cross-subsidy from industrial and through GUVNL’s hedging on coal procurement. Even so, the 2024 GERC order revised residential upward by 3.5%. Solar still works in Gujarat, payback is ~4.5 years for a 5 kW residential, but the marginal differential is thinner.

Uttar Pradesh (UPPCL): 4.8% residential CAGR and a long history of unreliable supply that makes self-generation valuable beyond pure rupee math. UPPCL’s 2024 tariff order added 6.2%. Solar payback in UP is now 3.8–4.2 years for a 5 kW post-Suryaghar.

Tamil Nadu (TANGEDCO): the highest residential CAGR at 5.5%. TANGEDCO’s tariff orders compress consumer pricing in the lower slabs but escalate aggressively in upper slabs (>500 kWh). Households consistently above 500 kWh/month face the steepest compounding. Solar payback for those households runs 3.5–4 years on a 5 kW system.

Karnataka (BESCOM): 3.8% residential CAGR, but commercial CAGR is 4.5% and industrial is 4.2%. BESCOM’s 2024 order added 4.0% for residential and 4.8% for commercial. For Bengaluru flats and independent houses, payback runs 4.5–5 years.

Sources: respective DISCOM published retail tariff orders 2014–2024, cross-validated against Central Electricity Authority tariff bulletins.

Commercial vs Residential Tariff Hike Patterns

Commercial tariff escalation runs ~1 percentage point faster than residential because cross-subsidy mechanics force commercial users to absorb a higher share of the DISCOM’s revenue gap. That is the structural reason every state’s commercial CAGR exceeds residential.

| Connection type | Avg CAGR 2014-24 | 25-yr bill multiplier (at observed CAGR) | Solar economics |

|---|---|---|---|

| LT Residential | 4.3% | 2.87× | Strong, PM Suryaghar accelerates payback |

| LT Commercial (shops, offices) | 5.1% | 3.46× | Very strong, AD compounds the case |

| HT Commercial (malls, IT parks) | 4.8% | 3.22× | Strong, open-access option further amplifies |

| LT Industrial | 4.2% | 2.81× | Moderate, depends on demand charge structure |

| HT Industrial | 3.8% | 2.55× | Moderate-strong with captive solar arrangements |

| Agricultural | 1.2% | 1.35× | Weak rupee case, subsidised tariffs distort math |

For a commercial owner running a 30 kW system with AD, the 25-year cumulative differential is typically ₹85 lakh–₹1.3 crore against grid. The drivers: higher commercial tariff today, faster escalation, AD tax shield that recovers ~40% of capex in years 1–2, and longer ownership horizons typical of commercial property.

If you run a commercial connection and have not modelled your tariff escalation in your last solar quote, you are almost certainly understating the 25-year differential. The commercial solar service page has the AD-adjusted ROI framework.

Common Mistakes Ignoring Tariff Escalation in Solar ROI

These are the recurring errors we see in customer-supplied ROI sheets and competitor quotes. Any one of them understates solar value by 20–40%.

-

1

Using today's tariff for all 25 years. This is the single most common error. It understates solar value by 30–40%. Always project at minimum 3% escalation; for most states 4% is closer to reality.

-

2

Ignoring fuel surcharge escalation. The FAC (Fuel Adjustment Charge) component of your bill compounds independently of the published tariff order. In Maharashtra 2024 it added 30 paise on top of the energy charge. Build it into your blended ₹/kWh.

-

3

Ignoring slab-jump effects. Your tariff hike is not uniform across slabs, DISCOMs hike upper slabs faster than lower. If you consume 450 kWh and a 4% hike pushes your bill into the next slab, your effective hike is closer to 7%. See [bill slab structures](/blog/solar-and-electricity-bill-slabs).

-

4

Discounting future savings at unrealistic rates. NPV (Net Present Value) discounting at 10–12% kills the future savings on paper. Use 6–7% for residential (matched to deposit rates) and 9–10% for commercial (matched to actual cost of capital). Higher rates are an analyst trick that biases against solar.

-

5

Assuming export tariff stays flat. APPC (Average Power Purchase Cost), what you get for exported units, does rise, but slower than retail (typically 1.5–2.5% CAGR). Model export at 2% escalation, not zero.

-

6

Forgetting AMC and replacement budget. A real LCOE includes ₹2,000–₹5,000/year AMC and a one-time inverter replacement at year 10–12 (₹25,000–₹50,000 for residential). Quotes that ignore these understate true LCOE by 15–20%.

-

7

Sizing only to current consumption. If your tariff is going to grow 2.7× over 25 years, your consumption profile will likely shift too (EV charging, AC penetration). Plan for [3 kW vs 5 kW vs 10 kW system sizing](/blog/3kw-vs-5kw-vs-10kw-home-solar) with 25-year load growth in mind.

A clean ROI sheet should explicitly show the escalation assumption on every page. If your vendor’s quote doesn’t, ask. If they push back, that quote is selling you a system on understated value.

Continue On-Grid vs Solar Insulation

Most households frame the decision as “spend ₹2.85 lakh today” versus “keep paying my bill”. That is the wrong framing, the real comparison is two long-term cash flows, one compounding upward (grid) and one flat (solar). Here is the honest pros and cons.

- + Generation cost locked at LCOE for 25 years

- + Every tariff hike becomes savings, not expense

- + PM Suryaghar subsidy cuts upfront 30–40%

- + Hedge against future EV / AC load growth

- + Property value uplift (₹40k–₹80k per kW installed)

- + Carbon offset ~1 tonne CO₂ per kW per year

- - Bill compounds ~52% over 10 years, ~167% over 25

- - Fuel surcharge adds independent volatility

- - Slab jumps as consumption grows accelerate cost

- - No fixed-rate option exists for residential users

- - Outage exposure (worse in UP, Bihar, parts of MH)

- - Zero hedge against future cross-subsidy changes

Verdict. For any household with monthly bills above ₹2,500 and a 10+ year ownership horizon, solar is the rupee-winning choice across every reasonable tariff scenario. For commercial connections above ₹15,000/month with AD applicable, the case is overwhelming, 25-year differentials run in tens of lakhs to crores. Stay on grid only if your bills are subsidised (BPL slab, agricultural), your horizon is under 5 years, or you have a roof that genuinely cannot host a system. Note: solar does not eliminate the bill entirely, see why solar bills are not zero for the detail.

How Heaven Green Energy Calculates Tariff-Adjusted ROI

Most solar quotes you receive, even from large brands, use a single static tariff for the entire 25-year projection. That is mathematically dishonest, and it leaves you with a payback number you cannot rely on. Heaven Green Energy runs every customer through a tariff-adjusted ROI model that reflects how your bill actually behaves.

The model uses:

- Three escalation scenarios: 3% conservative, 4% base, 5% upper-bound, so you see the range, not a single point.

- State-specific tariff trajectory: Maharashtra customers get MERC’s published 10-year pattern; Gujarat gets GERC’s; UP gets UPERC’s, etc.

- Slab-mix modelling: your consumption is mapped to the actual slab structure of your DISCOM, not a single blended rate.

- Realistic LCOE: including AMC, inverter replacement, and degradation at 0.5%/year.

- NPV at deposit-rate discount: 6.5% for residential, 9% for commercial, so future savings are valued honestly.

- Sensitivity tables: payback and 25-year cash flow at each of the three escalation scenarios.

We send the model output as a PDF report, year-by-year cash flows, payback in months, IRR (Internal Rate of Return), and NPV, before you commit. If the math doesn’t work for your specific case, we’ll say so.

Explore the services that match your situation:

- Residential Solar: 1–10 kW rooftop systems with PM Suryaghar subsidy and tariff-adjusted ROI modelling.

- Commercial Solar: 10 kW–1 MW with AD planning and 25-year tariff hedge structuring.

- Solar Calculator: instant estimate with 4% default escalation built in.

- Get a custom quote: three-scenario ROI report tailored to your bill.

Frequently Asked Questions

What is the average annual electricity tariff hike in India?

Indian electricity tariffs have hiked at 3.5–5.5% per year on average across the 2014–2024 decade, per Central Electricity Authority data and state regulator tariff orders. Residential averages 4.3% nationally; commercial averages 5.1%. Some states are higher, Tamil Nadu residential at 5.5% CAGR, UP at 4.8%, while Gujarat sits lowest at 3.2%. Decadal cumulative residential bill growth is roughly 40–55% depending on state.

Does solar protect against future electricity tariff hikes?

Yes, that is the core economic value of solar ownership. Your solar generation cost (LCOE) is fixed for 25 years at ₹2.50–₹3.50/kWh residential. Grid tariffs continue compounding at 3–6% annually. After payback (5–7 years for residential), every future tariff hike becomes savings on your side rather than expense. Over 25 years, a 5 kW residential system insulates roughly ₹22 lakh of cumulative bill exposure for a typical 600 kWh/month household.

How does a tariff hike affect solar payback period?

Tariff hikes accelerate solar payback rather than slow it. Your annual savings scale with grid tariff, while your LCOE stays flat. Roughly every 1% additional annual tariff escalation compresses payback by six months on a residential 5 kW system. A 5% escalation environment delivers payback ~8 months sooner than a 3% environment. The risk people fear, “what if tariffs stop rising?”, has zero historical precedent in India.

What is solar LCOE and why does it matter for tariff comparison?

LCOE (Levelised Cost of Energy) is the per-kWh cost of solar generation amortised across the full 25-year system life, including capex, AMC, inverter replacement, and degradation. For Indian residential rooftop in 2026, LCOE is ₹2.50–₹3.50/kWh after PM Suryaghar subsidy. For commercial with AD, ₹2.80–₹3.80/kWh. Because LCOE is fixed and grid tariff is rising, the gap between the two widens every year, that is the bill-insulation effect.

Why do commercial tariffs hike faster than residential?

Cross-subsidy. Residential tariffs are politically protected and the lower slabs are subsidised below cost. The revenue gap is recovered from commercial, industrial, and HT users through cross-subsidy surcharges. So when DISCOM costs rise, commercial bears a disproportionate share of the hike, typically 1 percentage point faster CAGR than residential. This is why commercial solar economics are even stronger than residential on a 25-year horizon.

Should I use today’s tariff or projected tariff to calculate solar ROI?

Always project, using today’s tariff for a 25-year calculation understates solar value by 30–40%. Use 3% escalation as a conservative floor, 4% as the base case for most states, and 5% for high-CAGR states like Tamil Nadu and UP. Any solar quote that runs static tariff math is selling you on a deliberately understated number. Ask your installer to share the escalation assumption on the quote page.

Does solar export tariff (APPC) also rise with tariff hikes?

APPC (Average Power Purchase Cost) does rise, but slower than retail, typically 1.5–2.5% CAGR versus 4–5% for retail. This widens the gap between what you save through self-consumption (retail tariff) and what you earn through export (APPC). It is one reason solar systems should be sized to maximise self-consumption rather than over-sized for export. The right size matches your daytime load, see 3 kW vs 5 kW vs 10 kW sizing.

What happens if I install solar but tariffs stay flat for several years?

Even in the unlikely zero-escalation scenario, a 5 kW residential system at LCOE ₹3.00/kWh still pays back in 6.8 years against a current tariff of ₹9/kWh, because the gap between today’s tariff and solar LCOE alone is ₹6/kWh. Escalation makes the case stronger; flat tariffs only weaken it modestly. Solar wins on absolute price gap, not just on escalation. The historical Indian record shows zero years of flat-or-falling residential tariffs since CEA records began.

Does PM Suryaghar subsidy change the tariff-insulation math?

Yes, it cuts upfront capex by ₹30,000–₹78,000 for residential, which directly lowers LCOE and accelerates payback by 1.5–2.5 years. After PM Suryaghar, residential LCOE drops from ₹4.50/kWh (unsubsidised) to ₹2.50–₹3.50/kWh. This widens the bill-insulation gap and keeps payback under 6 years even in lower-tariff states like Gujarat. The subsidy effectively means India’s central government is co-paying you to hedge against future tariff hikes.